Crixfeed is the focused digital media, crypto information Services Company for the decentralize crypto asset (DAX) and blockchain technology community.

Phone: +91-9111 318 318

Email: [email protected]

Web: crixfeed.com

This question has been asked by every futurist research lab in many of the largest banks, central banks, financial institutions, think tanks, consulting firms and government committees around the world.

R3CEV, a consortium effort financed by some of the world’s largest banks, is busy trying to answer this question. Goldman Sachs, McKinsey Consulting and Consumers’ Research have all written excellent reports on this question. The UK Government, the Senates of the US, Canada, Australia and the EU have all made inquiries along these lines.

Many startups also produce white papers concerning their particular innovation or use of blockchain technology, and often include the larger social question: “How this will change things?”

Much of this research underlines four major areas of change:

The digital revolution has totally transformed media, as we all know. It’s had an effect in the finance industry as well. Of course, financial institutions use computers. They used them for databases in the 1970s and 1980s, they made web pages in the 1990s and they migrated to mobile apps in the new millennium.

But the digital revolution has not yet revolutionized cross-border transactions. Western Union remains a big name, running much the same business they always have. Banks continue to use a complex infrastructure for simple transactions, like sending money abroad.

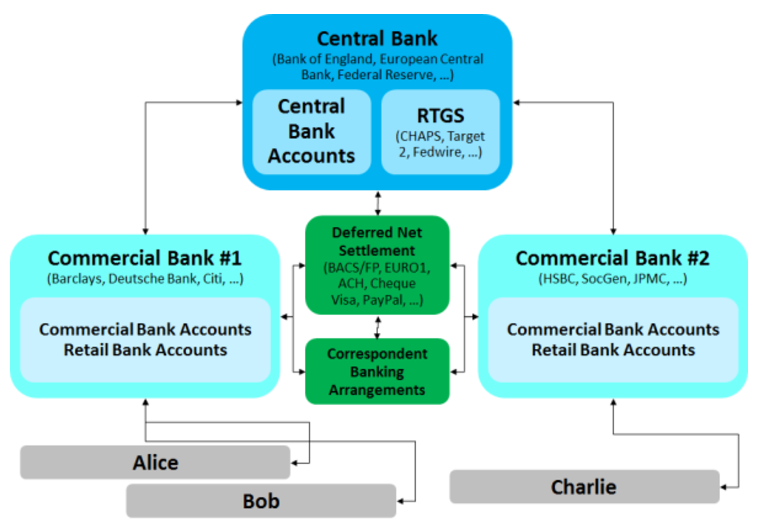

The following infographic, prepared by Richard Gendal Brown, shows the infrastructure and intermediaries in cross-border banking that have been in place since the ’70s.

This architecture is the result of the finance industry using highly secured private databases. Digitization has meant we merely sort information into private databases much faster.

Blockchain technology allows for financial institutions to create direct links between each other, avoiding correspondent banking. R3’s principal product to date, Corda, aims at correspondent banking. Corda is a play on words incorporating ‘accord’ (agreement) and ‘cord’ (the straightest line between two points in a circle).

In Corda’s case, the circle is made up of banks who would use a shared ledger for transactions, contracts and important documents.

Brown used to work on IBM’s blockchain products, but has since moved over to work at R3CEV.

Competing financial institutions could use this common database to keep track of the execution, clearing and settlement of transactions without the need to involve any central database or management system. In short, the banks will be able to formalize and secure digital relationships between themselves in ways they could not before.

In the above representation, that means correspondent banking agreements and the RTGS could both be shortcutted.

Transactions can occur directly between two parties on a frictionless P2P basis. Ripple, a permissioned blockchain, is built to solve many of these problems.

Bitcoin created something unique: digital property.

Before bitcoin, ‘digital’ was not synonymous with scarcity. Anything digital could be copied with the click of a button. A quick look at the music industry and album sales tells this story convincingly.

But bitcoin did something new: it created uncopyable digital code.

So, for the first time since bits and bytes were invented, there was a way to own something digital that couldn’t be copied. This gave the digital code value. To this day, bitcoin’s value is based on the capacity of its blockchain to prevent double-spending and the creation of counterfeit coins.

With this in mind, bitcoin developers have pioneered coloured coins that can act as stock in a company. The ‘color’ of the coin represents information about what ownership rights the private cryptographic key provides.

After receiving SEC permission, online retail giant Overstock announced it would issue public shares of company stock on its tØ blockchain platform. We’ve also seen the advent of ‘initial coin offerings’ (ICOs) and ‘appcoins’ (cryptocurrencies native to an app that help fund development of the project).

After receiving SEC permission, online retail giant Overstock announced it would issue public shares of company stock on its tØ blockchain platform. We’ve also seen the advent of ‘initial coin offerings’ (ICOs) and ‘appcoins’ (cryptocurrencies native to an app that help fund development of the project).

These examples are only part of the story for blockchains in digital assets. They can be the asset, but blockchains can also be used to run the market itself.

Basically, these efforts are treating digital assets as a bearer instrument, which is a wide and dexterous application.

This ability, however, extends beyond just recording transactions. Nasdaq, for example, was one of the first to build a platform enabling private companies to issue and trade shares using a blockchain.

Other developers are coding financial instruments that can be pre-programed to carry out corporate actions and business logic.

In 2016, a blockchain project called The DAO, running on the ethereum blockchain, was launched with the aim of emulating a crowdfunding market. Your percentage of contribution to the fund represented the percentage vote in how the total fund would be spent.

Blockchains can serve as a fully transparent and accessible system of record for regulators. The can also be coded to authorize transactions which comply with regulatory reporting.

For example, banks have severe reporting obligations to agencies such as FinCEN. Every single time they authorize a transaction of more than $10,000, they must report the information to FinCEN, who stores it for use as an anti-money laundering database.

With paper-world trading, the time frame for clearing and settlement of a transaction is generally referred to as ‘T+3’ - that is, three days after the trade (T), the transaction is settled.

With blockchain technology, the entire lifecycle of a trade - execution, clearing and settlement - occurs at the trade stage. With a digital asset, trade is settlement, and the cryptographic keys and digital ownership they control can lower post-trade latency and counterparty risk.

Whereas most databases are snapshots of a moment in time, blockchain databases are built from their own transaction history. They are a database with context, a history of itself, a self-contained system of record.

The implications for auditing and accounting are profound.